Stablecoins in B2B Payments: A Domestic Opportunity for U.S. Banks and Credit Unions

Overview

In high-volume or time-sensitive B2B workflows, U.S. corporations move tens of trillions of dollars every year through a combination of ACH, wires, checks, card rails, and treasury sweeps. This multi-rail environment can introduce coordination and reconciliation challenges that add complexity in managing liquidity efficiently.[1]

For leaders of U.S. banks and credit unions, stablecoins – digital currencies tied to stable assets like the U.S. dollar – present a powerful opportunity to modernize B2B payments. This blog explores how adopting stablecoin solutions can streamline domestic payment inefficiencies, reduce costs, and better meet the needs of business clients. It highlights verified domestic use cases and provides actionable steps to position institutions as leaders in the digital payments landscape.

Why Stablecoins Are Becoming Essential for Domestic B2B Payments

Stablecoins leverage blockchain technology to deliver speed, transparency, and cost efficiency, while maintaining stability typically associated with fiat currencies (i.e., government-issued money). These advantages are highly valuable for institutions handling B2B payments, driven by three key trends:

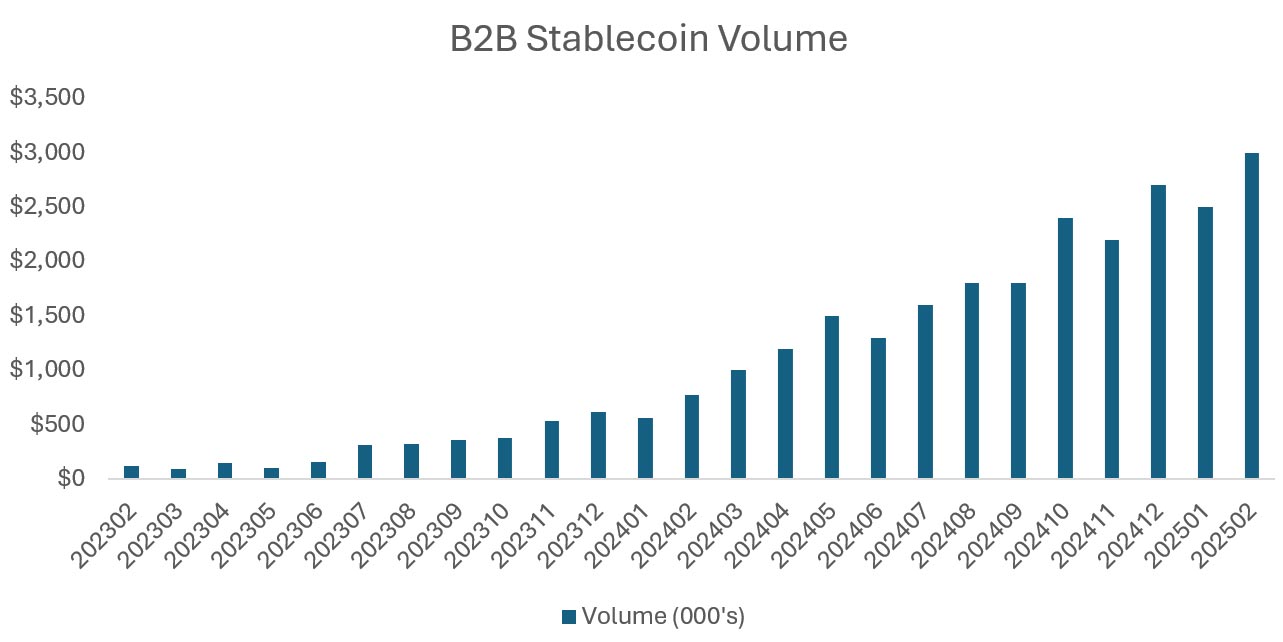

Source: Artemis Data Partners[8]

The following examples demonstrate how stablecoins are transforming domestic B2B payments, offering models banks and credit unions can adopt and emulate:

Recent federal legislation has established a regulatory foundation that enables U.S. financial institutions to support stablecoins, including the ability for subsidiaries to hold and issue stablecoins. However, this legislation is just the starting point. Evolving stablecoins into a mainstream B2B payment option requires additional work to build out the necessary supporting infrastructure, such as integration with existing systems, establishing compliance with anti–money laundering regulations, clarifying dispute rules, and educating clients on new terminology.

Fortunately, many of these required activities are similar to the efforts financial institutions and others have undertaken to bring previous payments to market. And, consistent with the playbooks used for those other payments, financial institutions do not have to wait until everything is built to start differentiating themselves in the market.

With proper investments in technology and common-sense guardrails, financial institutions are well positioned to begin bringing value to their customers by providing on- and off-ramps for stablecoins, offering custodial wallets, and even issuing and/or distributing other established and fully compliant stablecoins. By actively engaging in stablecoins today, banks and credit unions will solidify their competitive place in the market and position themselves for future success in the rapidly evolving digital economy.

We're shaping the future of B2B payments—and your input matters!

Help us identify the real-world barriers and opportunities for instant payments in your business. By completing this brief survey, you'll help guide the priorities of the Faster Payments Council's B2B Work Group.

Take the Survey Now: https://lp.constantcontactpages.com/sv/PyFHvCN/B2BWGSurvey

For leaders of U.S. banks and credit unions, stablecoins – digital currencies tied to stable assets like the U.S. dollar – present a powerful opportunity to modernize B2B payments. This blog explores how adopting stablecoin solutions can streamline domestic payment inefficiencies, reduce costs, and better meet the needs of business clients. It highlights verified domestic use cases and provides actionable steps to position institutions as leaders in the digital payments landscape.

Why Stablecoins Are Becoming Essential for Domestic B2B Payments

Stablecoins leverage blockchain technology to deliver speed, transparency, and cost efficiency, while maintaining stability typically associated with fiat currencies (i.e., government-issued money). These advantages are highly valuable for institutions handling B2B payments, driven by three key trends:

- Proven scale. Stablecoin transfer volume reached $49 trillion in 2025,[2] surpassing the combined volume of major retail card networks. While the majority of this $49 trillion represents crypto trading, roughly $10+ trillion[3] is non- trading, and up to 14% of that is B2B.

- Expanding liquidity. Total market cap stood at approximately $305 billion as of November 2025,[4] with forecasts projecting market cap growth of up to $4 trillion by 2030.[5]

- Evolving regulation. Federal legislation is beginning to provide clearer guardrails for adoption, with efforts such as the GENIUS Act[6] the CLARITY Act[7] helping to clarify the oversight of stablecoins. This has reduced perceived risk and encouraged industry investment.

- Reusability. Stablecoins have cash-like characteristics, and once issued, can be reused without having to off- and on-ramp with fiat. However, until broader acceptance occurs, there will still be a need for off-ramps and/or solutions where a debit card is tied to the stablecoin balance, offering point-of-sale functionality in local FX.

- Speed: Stablecoin transactions settle in minutes, providing near‑instant cash flow compared with the one‑to‑three‑day processing time for ACH or wire transfers, and opening the door for their use in high‑value, time‑sensitive U.S. B2B payments. U.S. instant payment rails provide comparable settlement speed, but unlike stablecoins, they are generally limited to domestic transactions. They also lack native programmability, which restricts automation and conditional‑payment capabilities.

Source: Artemis Data Partners[8]

- Cost Efficiency: Blockchain networks can facilitate transactions at minimal cost, creating new opportunities for efficiency within B2B workflows. When combined with automation, stablecoins can contribute to lowering overall payment management costs while working alongside existing rails.

- Transparency: Stablecoins are native assets on blockchain networks which record every transaction on an immutable ledger — a permanent, tamper-proof system. When payment details like invoice metadata or references are embedded and traced on-chain, it enhances transparency and accountability, meaning reduced disputes, minimized fraud, fewer audits, and greater trust in the payments ecosystem.[9] Leveraging ISO 20022 and e-invoice standards, which can be recorded off-chain and referenced on-chain, provides additional benefits as the amount of comprehensive and rich data and the sensitivity of it is not needed on-chain.

- Programmability: One of the most powerful features of stablecoins is their ability to embed rules and logic that automatically trigger payment-related actions based on non-payment related activities. For example, a stablecoin payment can contain a smart contract that releases payment to a supplier only when goods are delivered and verified. This automation can eliminate manual paperwork, automate early-pay discounts, and reduce delays, late fees, fraud, and disputes.[10]

The following examples demonstrate how stablecoins are transforming domestic B2B payments, offering models banks and credit unions can adopt and emulate:

- PayPal’s PYUSD for Corporate Payments: In September 2024, PayPal used its stablecoin, PYUSD, to settle invoices with U.S.-based vendors, streamlining accounts payable processes with faster settlement and lower costs.[11]

- Small Business Supplier Payments: Stablecoins like Circle’s USDC can be used to pay domestic suppliers and contractors, reducing settlement times from days to minutes and substantially cutting fees compared to wire transfers.

- Franchisee Settlements: Stablecoins can automate royalty payments for franchisee headquarters and franchisees by leveraging smart contracts for monthly transfers.

- Regional Cross-Border Efficiency: For U.S. businesses with North American suppliers, using USD stablecoins can simplify payments to international vendors without requiring FX (if the supplier prefers to keep or transact in USD) and can bypass costly correspondent‑banking fees.

- Intra-Day Liquidity & Cash Pooling: 24×7 token transfers settle in seconds and can be auto-reconciled on-ledger, optimizing liquidity management by removing dependency on wire cut-offs and periodic treasury sweeps between subsidiaries.

- Escrow & Milestone Invoicing: Smart-contract escrows can release funds automatically when Enterprise Resource Planning (ERP) triggers delivery, eliminating manual escrow accounts and letter-of-credit costs.

- Earned-Wage & Gig Payroll: Stablecoins can offer near-instant “Work-to-Wallet” settlement in tokenized dollars 24×7, offering an alternative to instant payments and Same-Day ACH by enabling continuous settlement outside of standard batch windows.[12]

Recent federal legislation has established a regulatory foundation that enables U.S. financial institutions to support stablecoins, including the ability for subsidiaries to hold and issue stablecoins. However, this legislation is just the starting point. Evolving stablecoins into a mainstream B2B payment option requires additional work to build out the necessary supporting infrastructure, such as integration with existing systems, establishing compliance with anti–money laundering regulations, clarifying dispute rules, and educating clients on new terminology.

Fortunately, many of these required activities are similar to the efforts financial institutions and others have undertaken to bring previous payments to market. And, consistent with the playbooks used for those other payments, financial institutions do not have to wait until everything is built to start differentiating themselves in the market.

With proper investments in technology and common-sense guardrails, financial institutions are well positioned to begin bringing value to their customers by providing on- and off-ramps for stablecoins, offering custodial wallets, and even issuing and/or distributing other established and fully compliant stablecoins. By actively engaging in stablecoins today, banks and credit unions will solidify their competitive place in the market and position themselves for future success in the rapidly evolving digital economy.

We're shaping the future of B2B payments—and your input matters!

Help us identify the real-world barriers and opportunities for instant payments in your business. By completing this brief survey, you'll help guide the priorities of the Faster Payments Council's B2B Work Group.

Take the Survey Now: https://lp.constantcontactpages.com/sv/PyFHvCN/B2BWGSurvey

[1] https://fasterpaymentscouncil.org/blog/15838/Getting-Paid-Faster-in-B2B-How-Instant-Payments-Help-Reduce-DSO-and-Improve-Access-to-Capital

[6] https://www.richmondfed.org/banking/banker_resources/news_flash/2025/20251118_genius_act#:~:text=Any%20issuer%20of%20payment%20stablecoins,of%20any%20payment%20stablecoin%20issuer.

[7] https://www.banking.senate.gov/newsroom/majority/the-facts-the-clarity-act#:~:text=FACT%3A%20The%20CLARITY%20Act%20Delivers,with%20a%20workable%20statutory%20framework.

Business Benefits of B2B Instant Payments Work Group

Thank you to the members of the FPC Business Benefits of B2B Instant Payments Work Group (B2BWG) who contributed to this blog.

B2B Instant Work Group Leadership

| Finzly | Dean Nolan (Chair) |

| Finvix Technologies | Andres Garbarini (Vice Chair) |

B2BWG Blog Primary Authors

| Finzly | Dean Nolan |

| SRM | Larry Pruss |

B2B Work Group - Additional Members

| 7T World LLC | Anthony Serio, Editorial Review |

| Alogent | Doug Hendricks |

| Euronet Worldwide | Rohan Bakshi |

| Euronet Worldwide | Audrey Blackmon |

| Euronet Worldwide | Romil Trivedi |

| Icon Solutions | Arjeh van Oijen |

| NAYA | Sherif Kozman |

| The Central Trust Bank | Sara Kerperin |

| ValidiFI | David Barber |

| Vments, Inc. | Steve Wasserman |

About the Business Benefits for B2B Instant Payments Work Group

Accelerate the adoption of instant payments for businesses by addressing key challenges and identifying best practices with B2B Instant Payments.

About the U.S. Faster Payments Council

The U.S. Faster Payments Council (FPC) is an industry-led membership organization whose vision is a world-class payment system where Americans can safely and securely pay anyone, anywhere, at any time and with near-immediate funds availability. By design, the FPC encourages a diverse range of perspectives and is open to all stakeholders in the U.S. payment system. Guided by principles of fairness, inclusiveness, flexibility, and transparency, the FPC uses collaborative, problem-solving approaches to resolve the issues that are inhibiting broad faster payments adoption in this country.